Clay Craft India IPO Details

Clay Craft India IPO is a 100% book-built issue comprising 54.24 lakh equity shares worth up to ₹110.11 crore, entirely a fresh issue of shares, with a face value of ₹10 per share. The company filed its DRHP with SEBI on September 2, 2025.

The price band of the issue is set at ₹193 to ₹203 per share and the lot size for an application is 600 shares. The minimum amount required by an individual investor (retail investor) is ₹2,43,600 (1,200 shares). The IPO will open from June 17 to 19, 2026, on the NSE SME platform, with a tentative listing date fixed as June 24, 2026. The book-running lead manager of the issue is HEM Securities Ltd., while the registrar to the offer is Kfin Technologies Ltd.

Clay Craft India IPO Date & Timeline

Clay Craft India Lot(s) Distribution

| Category | Lot(s) | Qty | Amount | Reserved |

|---|---|---|---|---|

| INDIVIDUAL | 2 | 1200 | 243600 | 1503 |

| sHNI | 3 | 1800 | 365400 | 143 |

| bHNI | 9 | 5400 | 1096200 | 287 |

Clay Craft India Reservation

| Category | Shares Offered | % |

|---|---|---|

| Total | 5424000 | 100% |

| Anchor | 1543800 | 28.46% |

| QIB | 1030200 | 18.99% |

| HNI | 774000 | 14.27% |

| INDIVIDUAL | 1803600 | 33.25% |

| Market Maker | 272400 | 5.02% |

Clay Craft India About

IPO Details

| Total Issue Size | 54,24,000 shares (aggregating up to ₹110.11 Cr) |

| Fresh Issue | 54,24,000 shares (aggregating up to ₹110.11 Cr) |

| Face Value | ₹10/- Per Share |

| Issue Type | Bookbuilding Issue |

| Listing At | NSE SME |

| Share Holding Pre Issue | 1,51,46,280 Equity Shares |

| Share Holding Post Issue | 2,05,70,280 Equity Shares |

| Reserved for Market Maker | 2,72,400 shares (aggregating up to ₹5.53 Cr) |

| Market Maker | Hem Finlease |

Key Performance Indicators(KPI)

| KPI | Mar-26 | Mar-25 | Mar-24 |

|---|---|---|---|

| ROE | 17.71% | 16.21% | 12.24% |

| RONW | 16.27% | 14.93% | 11.54% |

| EPS (BASIC) | 17.84 | 13.70 | 9.20 |

| P/E Pre IPO | 11.38 | ||

| P/E Post IPO | 15.46 |

About Company

Clay Craft India Ltd. (CCIL) is a manufacturer and distributor of ceramic tableware products in India, engaged in the design, development, production and sale of a wide range of ceramic tableware including dinner sets, tea and coffee serving sets, mugs, tumblers, platters, bowls, and table top accessories. Its product portfolio addresses the diverse requirements of retail consumers, institutional buyers, and the hospitality industry. The company markets products under its in-house brands, Clay Craft and JCPL, in addition to its proprietary brands, it has entered into arrangements with various customers for whom CCIL undertakes design, development, and manufacturing activities.

The company also offers customized ceramic solutions for corporate and institutional clients based on specific requirements and have developed a product range for the HoReCa (Hotel, Restaurant, and Catering) segment to meet the operational needs of the industry. CCIL’s capability to serve both broad-based and specialized demand segments, supported by its design and manufacturing infrastructure, enables it to operate across domestic and select international markets. As of March 31, 2026, it offers approximately 5770 stock-keeping units (“SKUs”) across various product categories under different brands. Mugs has a lion share, followed by Dinnerware and Tea/Coffee service sets in its total SKUs as well as in its revenue mix.

The company primarily operates on a business-to-business (B2B) model, supplying the majority of products through its own distribution network, large format retail chains and using different retail channels. The Company is committed to offering quality ceramic tableware at competitive prices and aims to foster long-term relationships with customers by adhering to industry standards and meeting specific business requirements.

As of March 31, 2026, its distribution network includes approximately 132 distributors across major states and union territories in India, supported by a dedicated sales and marketing team of 47 personnel. Over the years, it has developed and maintained long-standing relationships with distributors, large format retail chains and retailers, which has contributed to consistent market access and customer loyalty. In addition to traditional distribution, its products are available through other trade channels like, e-commerce marketplaces, and own websites. CCIL has also entered into commercial arrangements with large-format retail chains for the sale of its products through their outlets across India and with e-commerce platforms for online sales. As of the date of filing this offer document, it had 1392 employees on its payroll.

Issue Details / Capital History

The company is coming out with its maiden book building route IPO of 5424000 equity shares of Rs. 10 each to mobilize Rs. 110.11 cr. at the upper cap. The company has announced a price band of Rs. 193 - Rs. 203 per share. The minimum application to be made is for 1200 shares and in multiples of 600 shares thereon, thereafter. The IPO opens for subscription on June 17, 2026, and will close on June 19, 2026. The IPO constitute 26.37% of the post-IPO paid-up capital of the company. The shares will be listed on NSE SME Emerge. From the net proceeds of the IPO, it will utilize Rs. 97.00 cr. for capex on setting up of additional manufacturing facility at Manda, Rajasthan, and the rest for general corporate purposes.

The IPO is solely lead managed by Hem Securities Ltd., and KFin Technologies Ltd., is the registrar to the issue. HEM group’s Hem Finlease Pvt. Ltd., is the market maker, as well as a syndicate member.

After issuing entire equity capital at par value, the company issued bonus shares in the ratio of 2 for 1 in June 2025. The average cost of acquisition of shares by the promoters is Rs. 2.06, Rs. 2.54, Rs. 3.13, and Rs. 3.29 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 15.15 cr. will stand enhanced to Rs. 20.57 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 417.58 cr.

Financial Performance

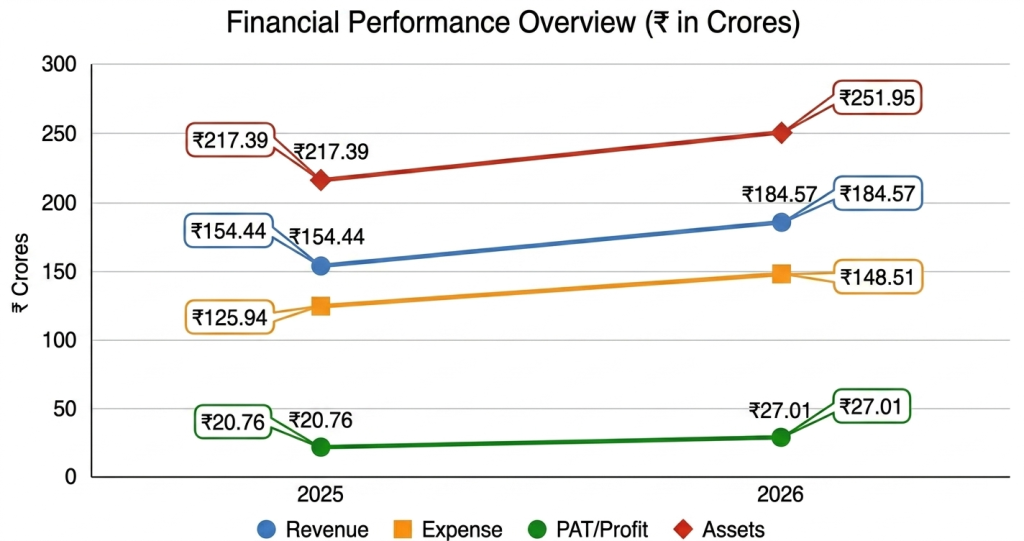

On the financial performance front, for the last three fiscals, the company has posted total revenue/ net profit, of Rs. 146.99 cr. / Rs. 13.50 cr. (FY24 – on standalone basis), and on consolidated basis, it marked Rs. 154.44 cr. / Rs. 20.76 cr. (FY25), Rs. 184.57 cr. / Rs. 27.01 cr. (FY26). The boosted profits from FY25 onwards (on a consolidated basis) raise eyebrows and concern over its sustainability as it is operating in a highly competitive and fragmented segment.

For the last three fiscals, the company has reported an average EPS of Rs. 15.02, and an average RoNW of 15.04%. The issue is priced at a P/BV of 1.85 based on its NAV of Rs. 109.64 per share as of March 31, 2026, but its post-IPO NAV data is missing from the offer documents.

If we attribute FY26 super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 15.46, and based on FY25 earnings, the P/E stands at 20.12. The issue appears aggressively priced, based on its recent bumper earnings, which may not be sustained. It is operating in a highly competitive and fragmented segment.

For the reported periods, the company has posted PAT margins of 9.28% (FY24), 13.66% (FY25), 15.02% (FY26), and RoCE margins of 14.42%, 16.69%, 18.26%, respectively, for referred periods.

All amounts in Indian Rupees crores

| Period Ended | Revenue | Expense | PAT | Assets |

|---|---|---|---|---|

| 2025 | ₹154.44 | ₹125.94 | ₹20.76 | ₹217.39 |

| 2026 | ₹184.57 | ₹148.51 | ₹27.01 | ₹251.95 |

Dividend Policy

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

Strength

Integrated and scalable manufacturing capabilities: Strong manufacturing infrastructure enables efficient production, quality control and scalability to meet growing demand.

Experienced promoters and management team: Industry experience and operational expertise support business growth and execution capabilities.

In-house design and product development: Dedicated focus on innovation, product design and quality enhancement helps the company cater to evolving customer preferences.

Risk Factors

Brand recognition risk: The company’s growth depends on maintaining and enhancing brand reputation, and any decline in brand perception may affect demand and profitability.

Supplier dependency risk: Dependence on key suppliers without long-term agreements may expose the company to raw material supply disruptions and operational challenges.

Changing consumer preference risk: Failure to adapt to evolving consumer tastes, design trends or quality expectations may adversely impact sales and market position.

To learn more about IPOs, the stock market, gold, cryptocurrency investments, and other topics, visit our website, newipo.info. Every piece of information on this website is thoroughly investigated by our staff before being made available to you. Investors can benefit from this in a number of ways.